| |

GST: Goods and Service Tax

The Goods and services tax is an indirect tax that has substituted several taxes in India, such as excise duty, VAT, services tax, and others. Specifically, the Goods and services tax is imposed on the supply of goods and services. GST is a complete, multi-phase; objective build tax charged on all the economic and value addition.

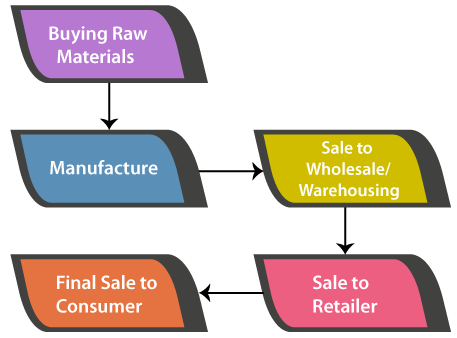

Multi-stage of ProductsThe products are passed from multiple handovers during their supply patterns beginning from producer till the final sale to the customer. Following are the phases:

The Goods and services tax is imposed on all the phases as mentioned above; it creates a multi-stage tax. Value Addition

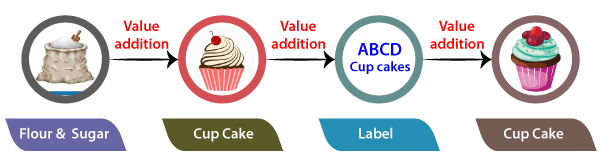

A producer of the cupcake company buys flour, sugar, and many other raw kinds of stuff for the manufacturing of the cupcake. The input amount rises when the sugar and flour are blended, and the cupcakes are prepared. The producer then sells all the cupcakes to the warehousing agent for the packaging of a large number of cupcakes in the cartons and labelling all the products. This is another valuable addition to the cupcakes. After this, the warehousing agent sells the product to the reseller. The retailer makes the packets of the cupcakes in smaller sizes and invests in the merchandising of the cupcakes, subsequently elevating their value. Goods and services tax is imposed on these value additions, i.e., the financial value added at every phase to attain the end sale to the consumer. Destination- BasedLet's consider the product manufactured in Kerala and sold to the final customer in New Delhi. Because the Goods and services tax is charged at the place of consumption, the complete tax proceeds will go to New Delhi and not Kerala. Goals of GSTIn this section of the article, we will discuss all the major goals of implementing 'Goods and Service Tax' in India. We will discuss all the goals also so that we can understand them in a much better way. Following are all the major goals of implementing GST in India: 1. To attain ideas of 'One Nation, One Tax'- Goods and services tax has substituted various pre-existing indirect taxes. The benefit of possessing one single tax implies that every state will pay the same amount for any particular product or system.

2. To include most of the indirect taxes in India- India had various preceding indirect taxes such as service tax, value-added tax, central excise, and many more that were imposed at several supply chain stages, and some taxes were directed by the state, and some by the centre and no combined and centralized tax on goods and services were there. Therefore, GST was initiated. Under GST, all prime taxes were included in a single tax. This eventually decreased the conformity pressure on taxpayers and made tax management easier for the government. 3. To reduce the domino effect of taxes- This was one of the basic aims of goods and services tax. Before, because of the multiple indirect tax rules, taxpayers were unable to set out the tax benefits of one tax against another one. For instance, the excise duties compensated while production couldn't be set off against the value-added tax unpaid over the marketing, which led to a ripple effect of taxes.

4. To restrain tax avoidance- GST laws in India are way stricter ascompared to any of the previous indirect tax rules:

5. To raise the taxpayer base- The introduction of GST has contributed to growing the tax base in India. Earlier, all the tax rules possessed different start bound for enrolment to depend on income.

6. Networked proceedings for the facility of doing business- Before, taxpayers suffered through much destitution while dealing with multiple tax officials under each tax rule. Other than this, while return filing was online, major assessments and paybacks processes occur offline.

7. Upgraded logistics and distribution arrangements- The unified tax system decreased the necessity of numerous documentations for the distribution of products. Goods and services tax has minimized shipment cycle times, upgraded supply series and reverse time, leading to the stockroom junction encompassed by several advantages.

8. To encourage competitive pricing and enlarge utilization- GST has increased the consumption and indirect tax proceeds. Because of the domino effect of taxes under the earlier reign, the cost of products in India was greater in comparison with global markets.

Merits of GSTAs we can see that, removing of cascading effect from the sales of goods and services is done by GST. GST has many advantages over the old tax regime, and due to its multi-sector merits, it was implemented over the old tax system in India. After cascading effect on sales of goods and services was removed, it has impacted the costs of goods. This is because GST eliminated the tax on already mentioned taxes; costs of Goods have decreased through it. Other than this, GST is also technologically driven mainly. GST accelerated many processes regarding technology-driven goods and services by providing a single window for activities like registration, application for a refund, response to the notice, and return filing on its portal. Following are the main highlighted merits of implementing GST over the old tax regime in India:

Components of GSTThere are three types of taxes pertinent under the GST system, which are as follows:

Under the GST law, all the three components of the GST that are mentioned above will be collected by the central government only (but it will depend upon that the transaction is inter-state or intra-state). We also have to note that GST is a destination-based tax in which the amount of tax is received by the state in which the product is supplied, not from the state where good is originated. To better understand the structure and implementation of all the different components of GST (as mentioned above), look at the following table structure:

Before GST: Tax laws in India before GSTIn the earlier regime of indirect taxes in India, there were many types of indirect taxes that were levied by both the state (where the transaction has happened) and the centre. Mainly taxes that were previously collected by states were in the form of VAT (Value Added Tax). Previously, every state in India had a different set of rules and regulations for collecting taxes on various goods and services. Before GST was implemented, the inter-state tax was collected by the centre in the form of Central State Tax (CST). Other than this, many indirect taxes such as local tax, octroi tax, and entertainment tax were charged together by centre and state. These multiple taxes were led to a lot of overlapping between the taxes charged by state and centre. There were many taxes that were charged by both state and the centre due to this overlapping in the taxes. Example: Earlier, when goods were manufactured and sold in a state, the states were charging Value Added Tax on them. Over VAT, the centre was also charging excise duty on it. This led to the tax on tax effect or cascading effect on various goods and services that we have discussed earlier. Following is the list of old tax regimes or list of various types of indirect taxes that were charged earlier before the implementation of GST in India:

Now, after GST was implemented all over India, all the above-listed taxes were replaced by SGST, CGST, and IGST. Note: Utilisation of 'Form C' after implementation of GST-regime:As we have discussed that GST implementation has replaced all the above-listed taxes that were earlier levied by centre or state or by both. But there are still some kinds of taxes or service charges that are charged by the centre or state in the form of 'Form C' utilization. Certain taxes which are still prevalent even after the implementation of GST-regime are charged in inter-state purchases made or transactions done, at a concessional rate of 2% by the utilization and issuing of 'Form C.' This method of charging tax is also applicable to certain goods that don't fall under GST-regime of charging tax, are as follows:

Other than this, the Utilisation of Form C is charging a concession rate of 2% is only applicable for the following inter-state transactions:

New compliances under GSTAs we have learned that we can fill online for the GST returns on many goods and services in the previous sections of this article. Also, apart from that, there are several new compliances that are introduced with the implementation of the GST-regime tax system. In this section, we will discuss the following new compliances that were introduced with the implementation of the GST tax system in India: E-invoicingIn India, the E-invoicing system for every transaction of goods and services was introduced with the GST implementation, and it became applicable from the 1st of October, 2020. This E-invoicing system became applicable to all the businesses that have an annual aggregated turnover of more than Rs. 5000000000 (Rs. 500 Crore) for any preceding financial years starting from the fiscal year 2018. Note: From January 1st, 2021, an amendment was made in this system, and E-invoicing was further extended to all the businesses that have an annual aggregated turnover of more than Rs. 100 Crore.Following is the working of the E-invoicing system under the GST regime:

Following are the highlighted points of the compliance of E-invoicing under the GST regime:

E-way billsWith the implementation of the GST regime in India, the 'E-way bills' system was also introduced, which was a centralized system of waybills. E-way bills system was introduced on 1st of April, 2018 for transactions of goods and services done under the inter-state. 2 weeks later, on 15th of April, 2018, for transactions of goods and services done under the intra-state in a stagged manner. Following are the highlighted points of the compliance of E-way bills system under GST-regime implementation in India:

Next TopicB.Sc - Bachelor of Science

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share